Creating Wealth Through Smart Investing and Disciplined Action

Investing and compounding are not just financial buzzwords—they’re the cornerstone of building lasting wealth. If you’ve explored these concepts in our earlier blogs, you’re already on the right track. But today, we’re diving deeper with insights from John Bogle’s The Little Book of Common Sense Investing. This timeless guide is packed with practical strategies to elevate your financial literacy and set you up for long-term success.

For me, discovering this book was a turning point. It came as a recommendation from a friend, and it sparked a personal finance journey that’s still shaping my decisions today. Now, it’s your turn to reflect: what financial goals are you striving for? Whether it’s financial independence, saving for a dream, or simply feeling secure, your goals act as your roadmap. Let’s explore how you can turn knowledge into action and make those dreams a reality.

What Financial Goals Are You Chasing?

Financial planning is about more than just saving for a car or a home—it’s about creating the life you truly want. For me, it’s the freedom to buy time. I see financial independence as the ability to take control of how I spend my days, free from the constraints of living paycheck to paycheck. It’s about having the resources to pursue passions, prioritize what matters most, and make decisions on my terms. Whether you aim for financial independence, increased savings, or steady financial gains, it all starts with a clear plan.

This is where The Little Book of Common Sense Investing by John Bogle becomes invaluable. Let’s explore five key takeaways that can help you achieve your goals.

Insights from The Little Book of Common Sense Investing

Broad-Market Portfolios: A Path to Diversification and Stability

Broad-market portfolios, such as S&P 500 index funds, provide a simple yet effective way to achieve diversification and mitigate investment risks. By giving you access to hundreds of companies spanning various industries, these funds reduce the impact of poor performance in any single sector, making your portfolio more stable in fluctuating markets.

This approach stands out for its ease of use. Instead of dealing with the intricacies of stock-picking, broad-market index funds allow you to participate in overall market growth. Since they replicate the performance of an entire index, these funds ensure your investments grow alongside the economy’s progress.

For a deeper dive into this topic, the case study “Are Index Funds Better Than Stock Picking?“ reveals some surprising findings that challenge the suggestions made in The Little Book of Common Sense Investing. The results showed that about 10% of companies currently listed on the S&P 500 grew 10x over the last decade—an outcome that might tempt investors toward individual stock-picking. However, there are important caveats to this finding, which are discussed in detail in the case study.

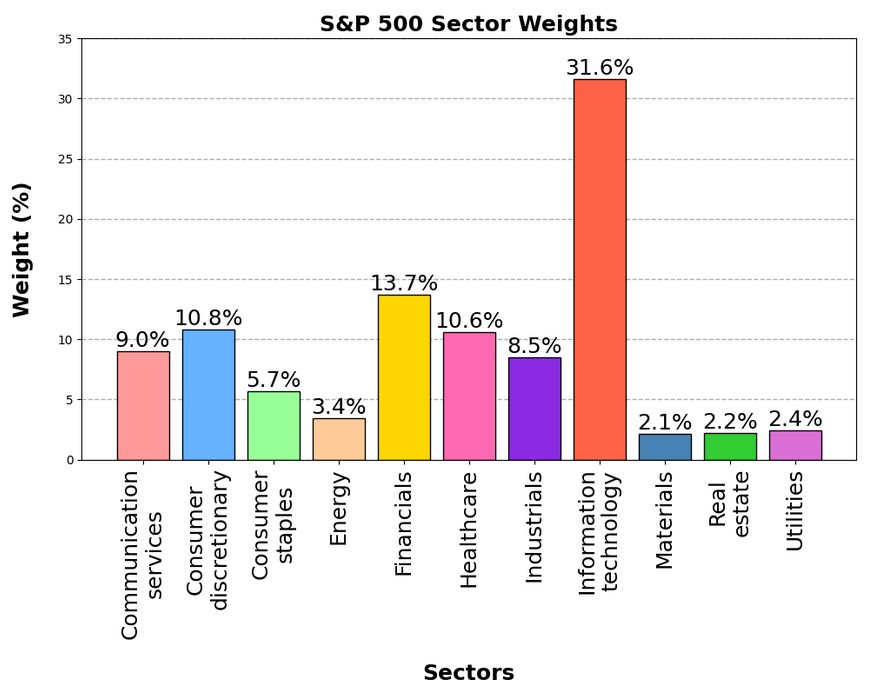

To complement this analysis, the accompanying plot illustrates the S&P 500 sector weights, offering a clear visualization of how diversification is achieved across industries. This data, sourced from the Pensions & Investments website, underscores the breadth of exposure provided by broad-market portfolios.

William Bernstein captures the essence of this strategy in The Four Pillars of Investing:

“Buy a well-run index fund and own the whole market.”

Such strategies encourage a disciplined, long-term investment outlook that supports steady portfolio growth, minimizes unnecessary risks, and aligns with the principles of sustainable wealth-building.

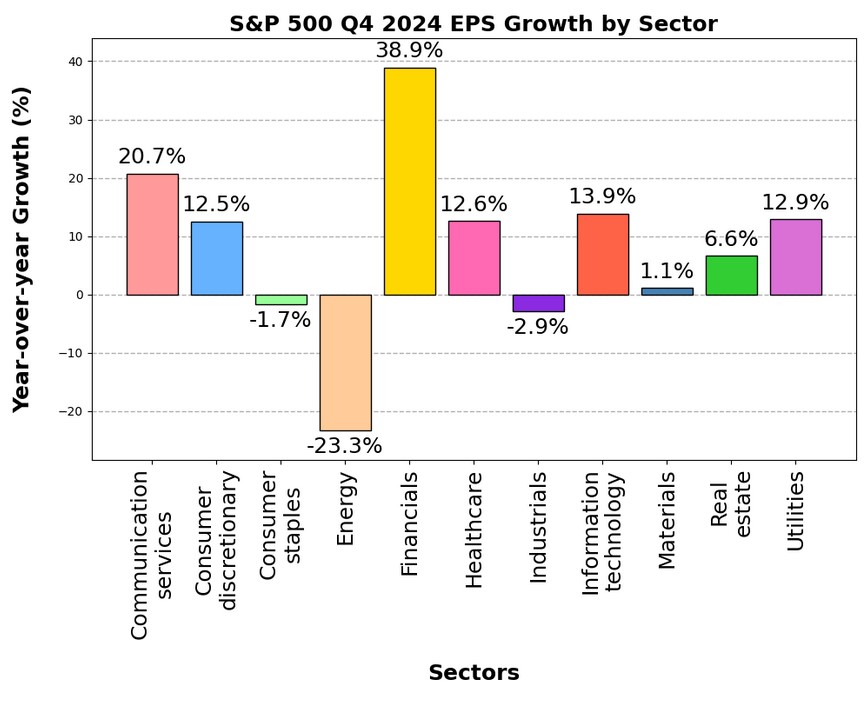

The importance of diversification becomes even more evident when examining sector-wise performance. The second plot (source: Pensions & Investments) highlights the S&P 500’s performance in Q4 2024, where the energy sector experienced significant declines. Investors focusing solely on energy companies would have faced substantial losses. In contrast, a diversified portfolio would have spread risk across other sectors, mitigating the impact of sector-specific downturns.

This example reinforces the resilience that broad-market portfolios provide, enabling investors to navigate fluctuations and maintain stability in their financial journey.

Minimizing Fees: A Crucial Element of Passive Investing

When it comes to investing, managing costs is often underestimated but critically important. High fees—whether from fund management or hidden expenses—gradually chip away at your returns, limiting your wealth-building potential over time. Every dollar spent on fees is a dollar lost to compounding.

In The Little Book of Common Sense Investing, John Bogle stresses that the costs tied to actively managed funds rarely justify their performance. Most active funds fail to outperform their benchmarks because fees undermine their gains. Similarly, Burton G. Malkiel, in A Random Walk Down Wall Street, emphasizes that low-cost index funds typically outperform managed portfolios by an average of 2% annually. This seemingly small margin compounds into significant wealth over decades.

Bogle’s observation sums it up perfectly:

“In investing, you get what you don’t pay for.”

By choosing low-cost index funds, you maximize the growth potential of your investments. Keeping expenses low isn’t just about saving money; it’s a core strategy for leveraging the power of compounding and accelerating long-term financial success.

Long-Term Investing: The Key to Tax Efficiency

Success in investing is not about quick gains but about staying committed for the long haul. Monish Pabrai illustrates this mindset with his advice:

“If you can stare at a wall for 30 minutes, you can be a great investor.”

Frequent trading, often triggered by short-term market swings, undermines your investment strategy. Not only does it expose you to emotional decision-making, but it also incurs capital gains taxes, which quietly drain your returns. Over time, these taxes can significantly weaken the compounding effect, one of the most powerful tools for building wealth.

Adopting a patient, long-term approach mitigates these challenges. Limiting unnecessary trades reduces your tax liabilities and allows compounding to operate uninterrupted. It also helps you stay focused on broader financial goals, avoiding distractions from market noise or short-term fluctuations.

Long-term investing isn’t just about holding onto assets; it’s about holding onto your confidence and strategy. By committing to proven principles and giving your portfolio the time it needs to grow, you enable steady, sustainable financial growth. Even modest beginnings can evolve into substantial wealth over time, offering you stability and peace of mind during market ups and downs.

Widening Financial Horizon: Don’t Put All Your Eggs in One Basket

While index funds offer a solid foundation of cross-section exposure, expanding your portfolio across various asset types and sectors can enhance financial resilience. A mix of stocks, bonds, and alternative investments ensures your portfolio isn’t overly reliant on any single market segment, balancing growth potential with stability.

Suggested Asset Allocation by Age

- 20s–30s:

80% stocks (growth-focused)

20% bonds (stability and risk mitigation) - 40s:

60% stocks (still growth-oriented but reducing risk)

30% bonds (greater emphasis on stability)

10% alternative investments (real estate, REITs etc) - 50s+:

50% bonds (income and capital preservation)

30% stocks (growth potential, albeit more conservative)

20% conservative assets (cash, annuities, or other low-risk investments)

Why This Matters:

As the saying goes, “Tailoring your investments to your age ensures your portfolio grows during your prime earning years and stabilizes as you approach retirement.” This age-based approach helps optimize growth during your younger years when you can take on more risk and shift toward stability and income generation as retirement nears, ensuring a secure financial future.

The Perils of Speculation and the Power of Discipline

One of the most essential lessons in investing is steering clear of speculation. As Benjamin Graham wisely observed in The Intelligent Investor:

“A little knowledge is a dangerous thing.”

Speculation often arises from the urge to chase market trends or make impulsive decisions. Unfortunately, these short-term reactions can derail long-term financial objectives and lead to avoidable mistakes.

John Bogle, in The Little Book of Common Sense Investing, emphasizes the importance of prioritizing simplicity and patience over the allure of quick gains. Emotional triggers like fear and greed drive speculation, whereas successful investing relies on discipline and adherence to time-tested principles.

Picture a horse wearing blinders—it avoids distractions and stays focused on the path ahead. Similarly, investors can benefit by ignoring market noise and following a well-researched plan. A practical strategy, such as investing in low-cost index funds, aligns your portfolio with long-term market growth while mitigating the risks associated with market timing and speculative trading.

Rather than reacting to every market movement, successful investing requires consistency and disciplined contributions. By resisting the temptation to speculate, you allow time and compounding to work their magic, setting the stage for lasting financial success.

Conclusion: The Path to Sustainable Wealth

Wealth-building isn’t about quick wins or secret formulas—it’s about showing up consistently, making informed decisions, and staying the course. Whether it’s investing in broad-market funds, keeping fees in check, or diversifying thoughtfully, every small action you take today is a step toward a more secure tomorrow.

Think of wealth creation as a steady climb, not a race. The most effective strategies are often the simplest: patience, discipline, and a clear vision of where you want to go. Start with one small step—be it setting up an emergency fund, reallocating your portfolio, or leveraging the power of compounding—and keep going.

Every move you make toward financial stability is an investment in your future self. So, why wait? Begin your journey today, and watch how the little things add up to something extraordinary. After all, the road to sustainable wealth starts with the steps you take now.

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Pingback: A Year of Insights: Canvas to Cosmos’ 2024 Review -