Personal finance isn’t reserved for the wealthy or financial experts—it’s a life skill for everyone. Imagine this: according to a recent study, nearly 70% of Americans have less than $1,000 in savings. Surprising, right? This statistic is more than just a number; it serves as a powerful reminder for all of us to take charge of our financial well-being.

This applies to everyone, regardless of their current circumstances. Whether you’re a:

- A college student juggling part-time jobs to pay off loans,

- A homemaker managing household expenses,

- A young professional handling your first paycheck, or

- Simply someone striving for financial independence,

Personal finance serves as the bedrock of success, with simple yet impactful principles that can transform your life when effectively applied.

A Relatable Start: The Piggy Bank Lesson

Remember saving up as a child for something special? Dropping coins into a piggy bank taught a simple yet vital lesson: financial discipline turns dreams into reality.

As we grow, financial responsibilities increase—tuition, rent, mortgages, and retirement savings—but the core principles of personal finance remain constant.

Real-Life Impact: A College Student’s Story

Consider my friend’s experience during his M.S. days. After a late night in the lab, he returns home to find that his roommate was hungry and out of cash. Waiting anxiously for funds from his father, he faced a problem many students share. This wasn’t just a lack of cash—the issue stemmed from insufficient financial literacy and poor money management skills.

Developing strong financial habits early can help avoid these challenges and establish a firm foundation for long-term stability.

Why Personal Finance Matters?

Personal finance goes beyond simply budgeting or setting aside part of your paycheck. It’s about:

- Creating Stability: Avoid living paycheck to paycheck.

- Building Freedom: Reduce financial stress.

- Seizing Opportunities: Achieve aspirations such as purchasing a home or rental property, starting a new business, or enjoying a comfortable retirement.

The Hidden Cost of Not Investing

Letting your money sit idle isn’t just missed growth—it’s losing value over time.

- Today vs. Tomorrow: $10,000 saved for a brand new car today might only afford a used car in 10 years due to inflation.

- Missed Opportunity: Investing that $10,000 at 6% annual returns could grow to nearly $18,000—enough to buy the car and cover extras.

Can Anyone Learn Personal Finance?

The Answer is Yes!

You don’t need to be a math genius or a finance expert. The basic principles are simple, and small changes can lead to significant results.

Example: The $4 Coffee Habit

Spending $4 daily adds up to:

- $120 monthly or $1,440 annually.

- Over ten years, that’s $22,334 with 8% compound interest—enough to buy a compact/economy car.

Consider saving or investing that money instead. Consistent, small actions taken today can yield substantial benefits in the future.

Budgeting: The Cornerstone of Financial Well-Being

What is it?

Budgeting is a financial strategy that monitors your income and expenses, helping you allocate resources toward necessities, discretionary spending, and savings.

How does it impact you?

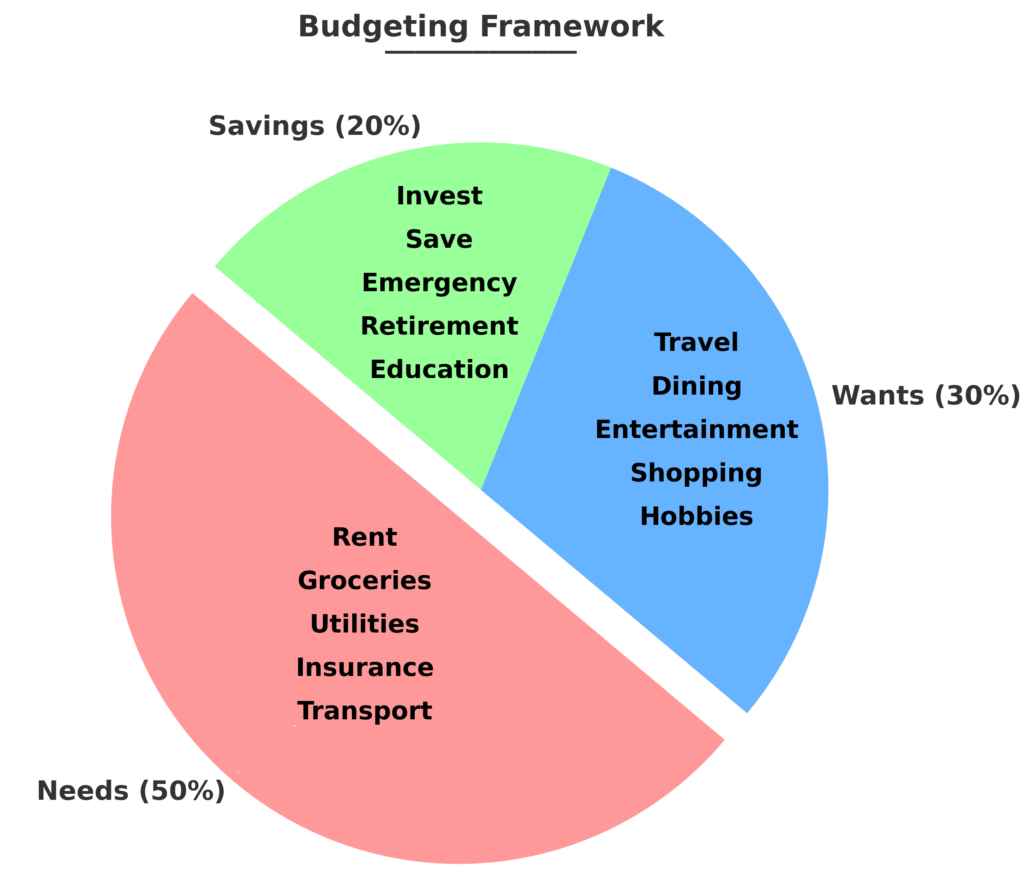

An effective budget enables you to control your expenses, steer clear of debt, and accomplish your financial objectives. By following frameworks like the 50/30/20 rule—50% for needs, 30% for wants, and 20% for savings or debt repayment—you can create a balanced financial life.

Simple way to do it:

Begin by monitoring all your expenses for a month. A strategy that works well for me is the concept of “paying yourself first,” a principle championed by financial experts like Robert Kiyosaki. Set aside 20% of your income immediately after payday—this way, you prioritize savings or investments without overthinking how to allocate the rest of your money. It’s a simple, effective way to build wealth with minimal effort.

Leverage budgeting tools or apps to categorize your spending and pinpoint areas for adjustment. Some examples are:

- For detailed planning: YNAB and EveryDollar.

- For families or couples: Goodbudget, Zeta, and Honeydue.

- For simplicity: Fudget

Build an Emergency Fund

What is it?

An emergency fund acts as a financial security measure, providing coverage for unforeseen expenses like house repairs, job loss, car breakdown, medical emergencies, or unexpected appliance failures.

How does it impact you?

Without an emergency fund, unplanned expenses can lead to debt or financial hardship. Having 6-12 months’ worth of monthly expenses in a high-yield savings account provides peace of mind and protects against life’s uncertainties.

Simple way to do it:

Automate a portion of your paycheck into a savings account. Start small and build consistently. Over time, you’ll create a robust safety net.

The Power of Savings

What is it?

Savings is the practice of consistently setting aside money to achieve future goals, such as funding education, starting a business, buying a home, or planning for retirement. It’s about building a financial foundation over time through disciplined effort.

How does it impact you?

Savings allows you to take control of your financial future by enabling greater flexibility and opportunity. Instead of relying on credit or loans, your savings can fund major life events or dreams, reducing financial stress. Over time, even small contributions can snowball, especially when invested wisely.

Simple way to do it:

Start early and save regularly. Set up automatic transfers into a dedicated savings account or investment account to take advantage of compounding. As Robert Kiyosaki said in Rich Dad Poor Dad, “Don’t work for money; make money work for you,” Invest wisely so your money works for you—not the other way around.

Choose the Right Deposit Accounts

What is it?

Choosing the right deposit accounts ensures your money is secure, accessible, and earning the best possible returns. Different accounts, like high-yield savings or CDs, are designed for specific financial goals. By aligning your accounts with your objectives, you can maximize efficiency and growth.

How does it impact you?

The type of account you choose has a direct impact on the growth of your savings. It also determines how quickly you can access your money. For example, high-yield savings accounts can generate higher returns than traditional savings accounts due to their typically higher interest rates. On the other hand, certificates of deposit (CDs) lock your money for a specific term. In return, they offer higher returns, making them ideal for long-term financial goals.

Simple way to do it:

Use high-yield savings accounts for accessible short-term savings and consider CDs for higher returns on funds you won’t need soon. For low-risk, long-term growth, explore treasury bonds.

Credit Cards: A Double-Edged Sword?

What is it?

A credit card is a financial tool that provides short-term borrowing with a credit limit, often offering perks like cashback or rewards but when not paid can cost you an interest of ~25%!

How does it impact you

When managed wisely, credit cards can help improve your credit score and earn valuable rewards. However, carrying a balance can result in high-interest charges, making credit cards a potential financial burden. For perspective, consider this simple example:

| Loan Type | Interest Rate(APR) | Principal($) | Interest Paid Over 1 Year ($) | Total Payment($) |

| Credit Card | 20% | 10K | 2K | 12K |

| Personal Loan | 10% | 10K | 1K | 11K |

Simple way to do it:

A key practice for responsible credit card use is to pay the entire balance in full each month to prevent the accrual of interest charges. Additionally, look for cards with rewards that align with your spending habits, such as cashback, travel points, or discounts.

Final Thoughts

Personal finance doesn’t have to be overwhelming. By mastering the basics—budgeting, saving, and understanding debt—you can establish a strong foundation for financial independence. As you become more confident, explore advanced strategies like investing in stocks, ETFs, real estate, and retirement accounts to build wealth and achieve your goals.

Remember, financial success isn’t about perfection. It’s about progress. Start small, stay consistent, and take complete control of your financial journey. Your future self will be grateful.

What are your thoughts on these strategies? Do you have any personal tips or experiences to share? Feel free to leave a comment or share your journey—we’d love to hear from you!

Disclaimer: This blog post is for informational purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

For your reading:

- Investing 101: Investing for Beginners

- What Is Personal Finance, and Why Is It Important?

- 8 Financial Tips for Young Adults

- The Best Budget Apps for 2024

- What Is a High-Yield Savings Account?

- Best Ways To Get Rid of Debt

Written by: Ankita Pujar & Dr. Robin Garg

Pingback: Money 102: Wealth-Building Strategies for Financial Growth

Pingback: Case Study: Are Index Funds Better Than Stock Picking? -

Pingback: How to Invest Like a Genius and Avoid Costly Mistakes

Pingback: A Year of Insights: Canvas to Cosmos’ 2024 Review -

Pingback: Think Like a Millionaire: Assets Liabilities and the Secret to Wealth - Canvas to Cosmos